Many homeowners find themselves grappling with the aftermath of water damage, which can lead to significant financial strain. Understanding the average insurance payout for such incidents is necessary for navigating the claims process effectively. In this guide, you will learn what factors influence these payouts, what to expect from your insurance policy, and how to maximize your compensation to cover repairs and restoration costs. By equipping yourself with this knowledge, you can better protect your financial interests when faced with water damage claims.

The Anatomy of Water Damage Claims

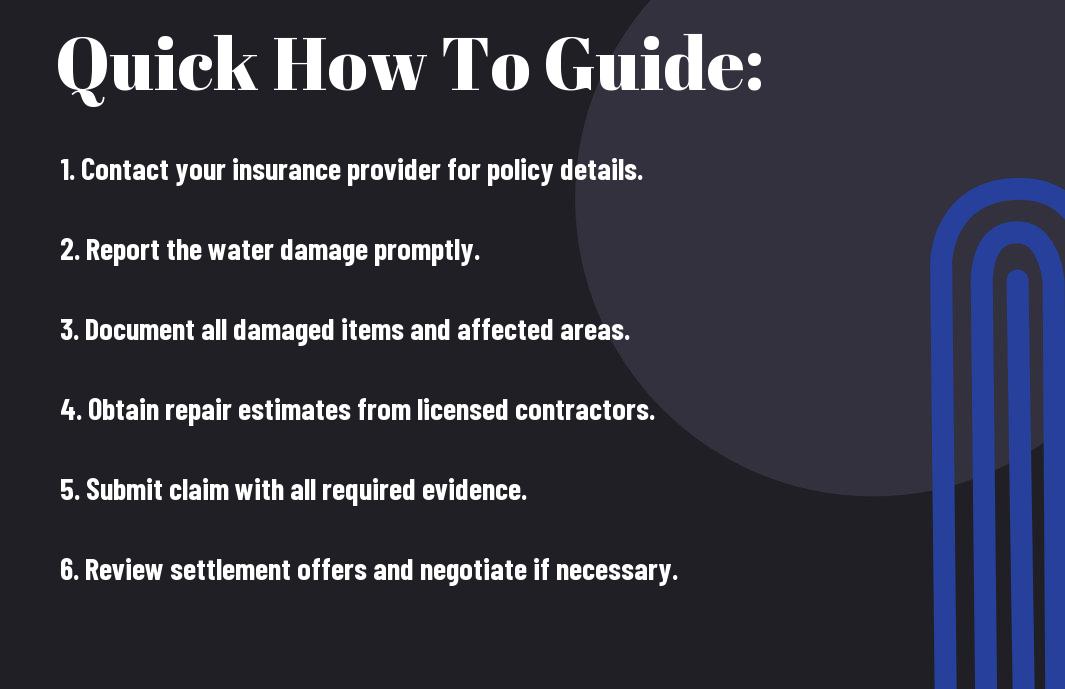

Understanding the anatomy of water damage claims is vital for homeowners navigating the complexities of insurance. Initiating a claim often requires a detailed inspection, documentation of damages, and communication with your insurance provider. Familiarizing yourself with the claims process can expedite resolution. Factors such as the cause of water damage, policy limits, and coverage specifics will influence the payout amount you can expect. For more information on what your homeowner’s insurance might cover, check out Does Home Insurance Cover Water Damage? (2025).

Common Causes of Water Damage

Water damage can stem from various sources, each with potential implications for your insurance claim. Common causes include burst pipes, leaks from appliances, natural disasters like floods, and roof leaks. Each cause may not only affect the coverage available under your policy but also how you go about filing your claim.

Key Terminology in Insurance Policies

Familiarizing yourself with key insurance terminology can empower you during the claims process. Terms like “deductible,” “exclusions,” and “coverage limits” are vital to understanding your policy. Knowing the definitions of these terms helps you navigate the nuances of your coverage and avoid surprises when filing claims for water damage.

Diving deeper into these terms, “deductible” refers to the amount you must pay out-of-pocket before your insurance kicks in. “Exclusions” are specific situations not covered under your policy, which might leave you vulnerable to certain types of water damage. Additionally, “coverage limits” indicate the maximum amount your insurer will pay for a particular loss. Understanding these details empowers you to make informed decisions regarding your policy and claims.

Factor Analysis: How Insurers Calculate Payouts

Insurers rely on a variety of factors to determine water damage payouts. These include the specific insurance policy you hold, the cause of the water damage, and the extent of the damage itself. Each claim is assessed on its unique merits, with adjusters evaluating the costs of repairs and how they align with the coverage limits of your policy. By understanding this evaluation process, you can better navigate your claim and ensure a fair reimbursement.

Evaluating the Extent of Damage

Assessing the extent of damage involves a thorough inspection of affected areas to identify both visible and hidden issues. Insurers look for signs such as mold growth, structural damage, or damage to personal property. You may need to provide documentation, such as photos or repair estimates, to help adjusters accurately gauge the severity of the situation. This step is pivotal in influencing your final payout amount.

Understanding Replacement Costs vs. Actual Cash Value

Your insurance policy may cover either replacement costs or actual cash value (ACV) when it comes to water damage claims. Replacement cost refers to the amount needed to replace damaged items with new ones of similar kind and quality, without depreciation. In contrast, ACV represents the item’s original value minus depreciation, which can significantly impact your payout. Understanding this difference is vital for managing expectations regarding your claim.

Replacement costs typically lead to higher payouts since they account for the current market price of new items. For instance, if a water-damaged carpet originally cost $1,000 but is now worth $600 due to wear and tear, an ACV policy would only reimburse you $600. However, a replacement cost policy would provide the full $1,000 necessary to buy a comparable carpet. Carefully reviewing your policy terms will help you determine which coverage applies and how it impacts your financial recovery after a water damage incident.

Real-World Averages: What to Expect

Understanding real-world averages for insurance payouts can significantly aid you in preparing for potential water damage claims. While individual circumstances vary, having general expectations can help mitigate surprises and guide your recovery efforts. Insights from data reveal the breadth of average payouts across different scenarios, empowering you with knowledge for future incidents.

National Averages for Insurance Payouts

On a national scale, the average insurance payout for water damage typically ranges from $20,000 to $30,000. However, some incidents may lead to payouts far exceeding this range, especially in cases of extensive flooding or major structural issues. Knowing this baseline helps set your budget for repairs and restoration.

Regional Variations and Influencing Factors

Regional variations play a substantial role in determining insurance payouts for water damage. Geographic factors, such as local weather patterns and historical flooding incidents, contribute significantly. For instance, areas prone to hurricanes or heavy rainfall may see higher premiums and subsequent payouts due to increased risk. Additionally, local building codes and construction practices can influence the extent of damages and necessary repairs.

- Geographic location impacts risk assessment and payout potential.

- Building codes dictate costs and may vary across regions.

- Higher risk areas tend to have higher insurance premiums.

- Average payouts can vary widely from state to state.

- Thou must consider these factors when evaluating your own coverage and claims.

The interplay of these regional factors can introduce complexities in your claim process. For example, if you reside in a flood-prone area, your insurer may charge higher premiums to offset the predicted costs of payouts. Alternatively, if your home was constructed with water-resistant materials, you might experience lower damage severity during an event, resulting in a different payout scenario. Understanding these regional impacts allows you to tailor your insurance coverage effectively.

- Local building practices can minimize or exacerbate water damage.

- Climate change’s impact may influence future regional risk.

- In-depth knowledge of your area’s insurance landscape benefits you.

- Consulting with reputable agents can guide policy adjustments.

- Thou should always review your home’s risk factors regularly.

Maximizing Your Payout: Insider Tips

Securing the highest possible payout for water damage requires strategic planning and knowledge of the claims process. To bolster your case, consider these tips:

- Document all damages thoroughly.

- Keep receipts for all repairs and mitigation efforts.

- Be consistent and honest in your communication.

- Follow up regularly regarding your claim status.

Knowing these strategies can significantly enhance your likelihood of receiving a generous payout.

Documentation and Evidence Collection

Gather comprehensive documentation to support your claim. Take photographs of water damage, keep records of repairs, and retain any invoices related to mitigation efforts. The more evidence you present, the stronger your case becomes, making it difficult for the insurance company to dispute your claim.

Working with Insurance Adjusters Effectively

Effective communication with insurance adjusters can streamline the claims process. Since adjusters are responsible for evaluating your claim and determining the payout, addressing their queries promptly and thoroughly is important. Provide all necessary documents and maintain a professional demeanor for a favorable assessment.

Presenting your case effectively hinges on your ability to forge a cooperative relationship with the adjuster. Remain transparent about the damages and any necessary repairs, and don’t hesitate to ask clarifying questions if you encounter jargon or complex terms. Being proactive in discussions allows you to guide the adjuster in understanding the full extent of your damages. Additionally, staying organized will equip you to quickly address any follow-up inquiries that arise during the evaluation process, ensuring your claim remains a priority. Keep the lines of communication open for a smoother negotiation process.

The Future of Insurance Payouts for Water Damage

As the frequency and intensity of water damage incidents increase due to climate change, insurance companies are likely to reassess their coverage policies. Enhanced risk models and real-time data could result in more personalized premiums and payouts that reflect actual risk levels. Innovations in claim processing and policy adjustments will likely shape how you experience insurance claims. Exploring experiences on forums like Water damage insurance claim – flooring & how many … provides invaluable insights into these evolving processes.

Trends in Policy Changes and Coverage

Many insurance providers are adapting their policies to respond more effectively to widespread water damage claims. This can lead to higher deductibles for certain risk categories or the introduction of additional coverage options specifically tailored for flooding and other water-related issues. Staying informed about these changes can help you modify your coverage accordingly to better protect your assets.

Technological Advances Affecting Claims Processing

Technology is revolutionizing how insurance claims for water damage are processed, leading to faster approvals and payouts. Insurers utilize artificial intelligence, machine learning, and data analytics to assess damage and expedite claims efficiently. Moreover, mobile apps empower you to file claims, upload photos, and track the status of your request in real-time, enhancing overall customer experience.

Impact of Technology on Claims Processing

Advanced technologies are streamlining the entire claims process. For example, drones can now survey damage from above, providing insurers with quicker assessments without necessitating an in-person visit. Automated systems analyze the submitted data and determine payout eligibility, substantially reducing processing times. Insurers equipped with these technologies can significantly enhance your experience, minimizing the hassle and uncertainty commonly associated with water damage claims. These innovations can also contribute to more accurate payout assessments, ensuring you receive a fair compensation based on actual damage incurred.

To wrap up

Drawing together the information on water damage insurance payouts, you can expect an average payout ranging from $2,500 to $12,000, depending on various factors such as the severity of the damage and your specific policy coverage. It’s necessary to review your insurance documents to understand the details of your coverage. By being aware of these averages, you can better prepare yourself for potential water damage claims and ensure you have adequate protection for your property.

FAQ

Q: What factors influence the average insurance payout for water damage?

A: The average insurance payout for water damage can vary significantly based on several factors. These include the type of water damage, whether it’s caused by a covered peril (such as a storm, burst pipe, or appliance malfunction), the extent of the damage, the limits of the policyholder’s coverage, and any applicable deductibles. Additionally, the geographical location of the property may play a role, as areas prone to flooding or other water-related incidents may have different average payouts compared to those with less risk.

Q: How can I estimate the potential payout for my water damage claim?

A: To estimate the potential payout for your water damage claim, start by reviewing your insurance policy to understand the coverage limits and exclusions. Next, document the extent of the damage with photographs and written descriptions. Gather quotes from contractors for the repairs needed, which can help establish the financial impact. It’s also beneficial to consult with your insurance adjuster, as they can provide insights into how much similar claims have yielded and what specifics may affect your payout.

Q: Are there any limitations that could reduce my insurance payout for water damage?

A: Yes, several limitations could reduce your insurance payout for water damage. These may include your policy’s deductible, which is the amount you must pay out of pocket before insurance coverage kicks in. Certain types of water damage, like flooding, may not be covered unless you have specific flood insurance. Additionally, any damages resulting from neglect, lack of maintenance, or policy violations could also lead to a reduced payout or denial of the claim. It’s important to understand your policy details to avoid unexpected limitations during the claims process.