Most insurance claims are submitted with the hope of receiving support when you need it most. However, claims can sometimes be denied, leaving you frustrated and confused. Understanding the two main reasons for a claim denial can empower you to navigate the process more effectively. This post will investigate into these reasons, helping you grasp the rules governing your claim and how to improve your chances of approval in the future.

Identifying Incomplete Information as a Claim Denial Factor

Incomplete information is one of the primary reasons claims face denial. Often, you may think your submission is thorough, but missing details can result in automatic rejections. For a complete list of Common Reasons for Insurance Claims Denials, understanding what constitutes incomplete documentation is vital to ensure your claim is processed smoothly.

Documents That Often Fall Short

Your claims can be denied if specific documents are missing or inadequately filled out. Common culprits include insufficient medical records, incomplete claim forms, or lack of proper signatures. If important details like diagnosis codes or treatment dates are not included, the insurer may see the claim as invalid.

How Incomplete Submissions Lead to Rejections

Incomplete submissions often lead to rejections because insurance companies rely on comprehensive documentation to process claims efficiently. If you fail to provide necessary information or fail to follow submission protocols, your claim may be marked as inadequate. This lack of information can result in misunderstandings regarding the services provided or the necessity of specific treatments, prompting a denial based on insufficient evidence.

When documentation falls short, insurers are unable to assess the merit of your claim properly. Even a missing signature on a form can lead to rejection, which is frustrating after you’ve submitted what you thought was a complete package. Each element of your claim serves a purpose, contributing to the total picture; without it, the insurer may rule against you. Always double-check that all required paperwork is included and that every detail is accurate to avoid this common pitfall.

The Impact of Coverage Limitations on Claim Approvals

Coverage limitations significantly influence whether your claim gets approved. Insurance policies often contain caps on payouts for specific incidents, meaning that if your damages exceed these limits, your claim may face denial or reduced compensation. For instance, if your policy stipulates a maximum payout of $10,000 for water damage, but the costs amount to $15,000, the insurer will likely only cover a portion of the expenses based on your policy terms, leaving you with substantial out-of-pocket costs.

What Policy Exclusions Mean for Your Claims

Policy exclusions outline specific situations or damages that are not covered under your insurance. If your claim involves an excluded peril, such as flood damage in a standard home insurance policy, it will be automatically denied. Understanding these exclusions is vital in managing your expectations and ensuring that you’re adequately protected against common risks.

Navigating Policy Details: Key Areas to Review

Focusing on the details of your insurance policy can reveal potential pitfalls that could result in claim denials. Look closely at the exclusions, coverage limits, deductibles, and conditions that apply to your policy. For instance, some policies require that you maintain your property regularly to avoid coverage inconsistencies.

Delving into the specifics of your policy can uncover critical areas that may affect your claim. Analyze the fine print concerning ‘Acts of God,’ often listed as exclusions or conditions under which coverage may be limited. Also, review any endorsements or additional riders you may have, as these could expand or restrict coverage significantly. Keep a checklist of these items handy to ensure you don’t overlook anything, and always ask your agent about unclear sections or ambiguous language that could impact your claims processing.

Analyzing the Role of Claims History

Your claims history can greatly influence the outcome of current or future claims. Insurers often assess this history to determine whether you are a higher risk. Frequent claims or a history of denied claims may signal to insurers that you are more likely to file subsequent claims, which can lead to a denial or lesser coverage. To gain insight into your claims history and how it impacts your coverage, you can refer to the Common Reasons Insurance Claims Are Denied and How … blog post.

The Influence of Prior Claims on Future Denials

Understanding the Claims Process from an Insurer’s Perspective

Strategies for Strengthening Your Claims

Developing effective strategies can greatly enhance the likelihood of your claims being approved. Focus on clear communication, comprehensive documentation, and maintaining a collaborative relationship with your insurer. By employing these tactics, you can minimize misunderstandings and navigate the claims process more smoothly, potentially averting issues that lead to denials.

Essential Tips for Comprehensive Documentation

Thorough documentation is vital to the success of your claim. Maintain organized records that detail all communications, incidents, and evidence related to your claim. Key elements to include are:

- Clear descriptions of events leading to the claim

- Photographic evidence, if applicable

- Invoices and receipts for any relevant expenses

- Witness statements, if necessary

- Your insurance policy and any applicable endorsements

Any lack of detail in your documentation can leave room for doubt, making your claim vulnerable to denial.

Best Practices for Engaging with Your Insurer Effectively

Engaging positively with your insurer sets a collaborative tone for the entire process. Clear and open communication helps to build rapport, enabling you to address issues before they escalate. Be prompt in providing any additional information they request, and take detailed notes during discussions to clarify any complex points. Always follow up on unanswered inquiries and ensure you understand their timelines and requirements for the claim process. When you approach your insurer with professionalism and attentiveness, you’re more likely to foster a supportive relationship that facilitates the approval of your claim. This proactive attitude exhibits your commitment to a fair resolution, which can often sway decisions in your favor.

The Claims Review Process: Insights for Policyholders

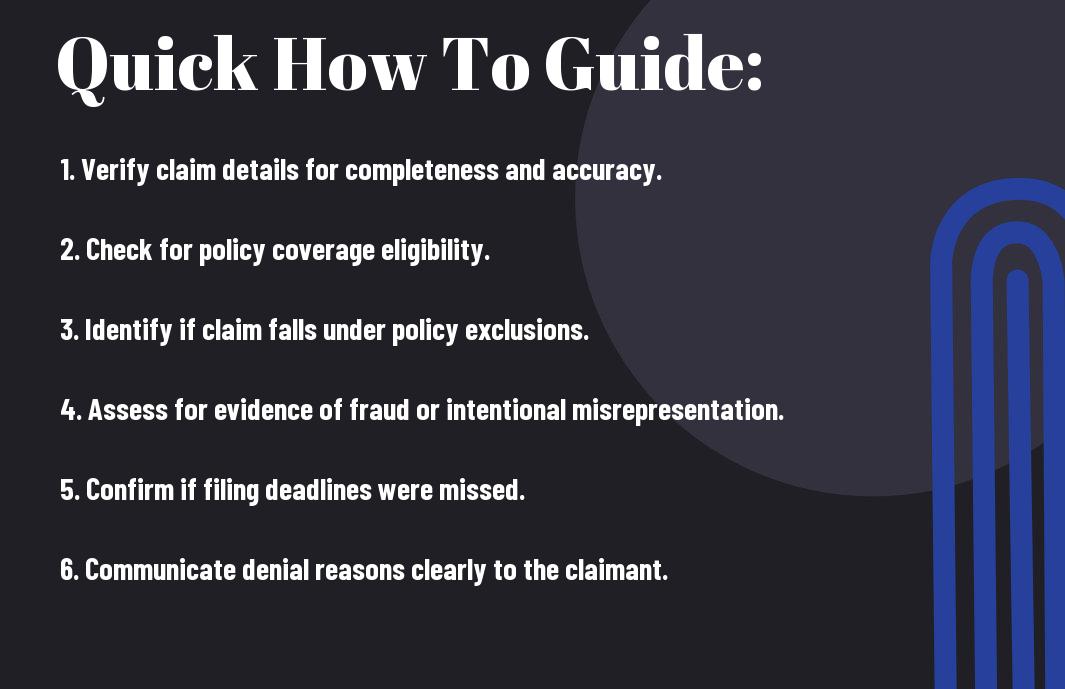

The claims review process is pivotal in determining the outcome of your submitted insurance claim. Insurers typically follow a systematic approach, analyzing the details of your claim against the policy’s terms and conditions. During this review, they evaluate documentation, assess the validity of your claim, and may even conduct further investigations to ensure the legitimacy of the request. By understanding this process, you can better prepare your submissions and avoid common pitfalls.

How Insurers Assess Claims and Common Pitfalls

Your claim undergoes thorough scrutiny as insurers assess the facts, supporting documents, and the incident’s alignment with your policy. Common pitfalls include submitting incomplete documents or failing to provide necessary evidence, like photographs or witness statements. Ensuring you have all required information and that it clearly supports your claim is vital for a favorable review.

The Importance of Clear Communication in Claim Submissions

Clear communication in claim submissions fosters understanding and expedites the review process. Vague descriptions or technical jargon can lead to confusion or misinterpretation, which may delay your claim’s approval or result in denial. Presenting details in straightforward language while clearly outlining your request and circumstances is important for guiding claim adjusters toward a swift resolution.

Effective communication not only enhances the clarity of your claim but also builds a relationship of trust with your insurer. By being concise and straightforward, you pave the way for faster inquiries and responses. For instance, using bullet points to summarize key facts can help adjusters quickly grasp important information, while well-documented evidence reinforces your narrative. Following up periodically to provide additional information or to clarify any questions can show your commitment and seriousness about the claim, encouraging the insurer to prioritize your case.

Summing up

With this in mind, the two main reasons for denying a claim typically revolve around insufficient documentation and failure to meet policy terms. You should ensure that all necessary paperwork is submitted accurately and that your claim aligns with your insurance coverage. For deeper insights and tips to strengthen your claims process, check out Medical Claims 101: How to Avoid Common Denial and ….

Q: What are the common reasons for denying an insurance claim?

A: Claims can be denied for various reasons, with two of the most prevalent being lack of coverage and failure to meet policy conditions. Lack of coverage occurs when the claim falls outside the scope of what the policy provides for, such as a specific event not being included. Meanwhile, failure to meet policy conditions can happen if the insured did not adhere to the required steps, such as timely reporting the claim or providing necessary documentation, which can result in denial.

Q: How can insufficient documentation lead to a claim denial?

A: Insufficient documentation is a frequent reason for denying a claim because insurance companies require specific evidence to support the claim. If the claimant fails to provide necessary paperwork, such as receipts, incident reports, or proof of ownership, the insurer may not have the means to validate the claim. Therefore, ensuring that all requested documents are submitted correctly and on time is vital for the approval process.

Q: What impact do policy exclusions have on claims?’

A: Policy exclusions outline particular situations or damages that are not covered under the insurance policy. Common examples include pre-existing conditions in health insurance or flood damage in homeowners’ insurance. If a claim is filed for an event that falls under an exclusion, it will likely be denied. Therefore, it’s important for policyholders to thoroughly review their insurance documents to understand what is and isn’t covered before filing a claim.