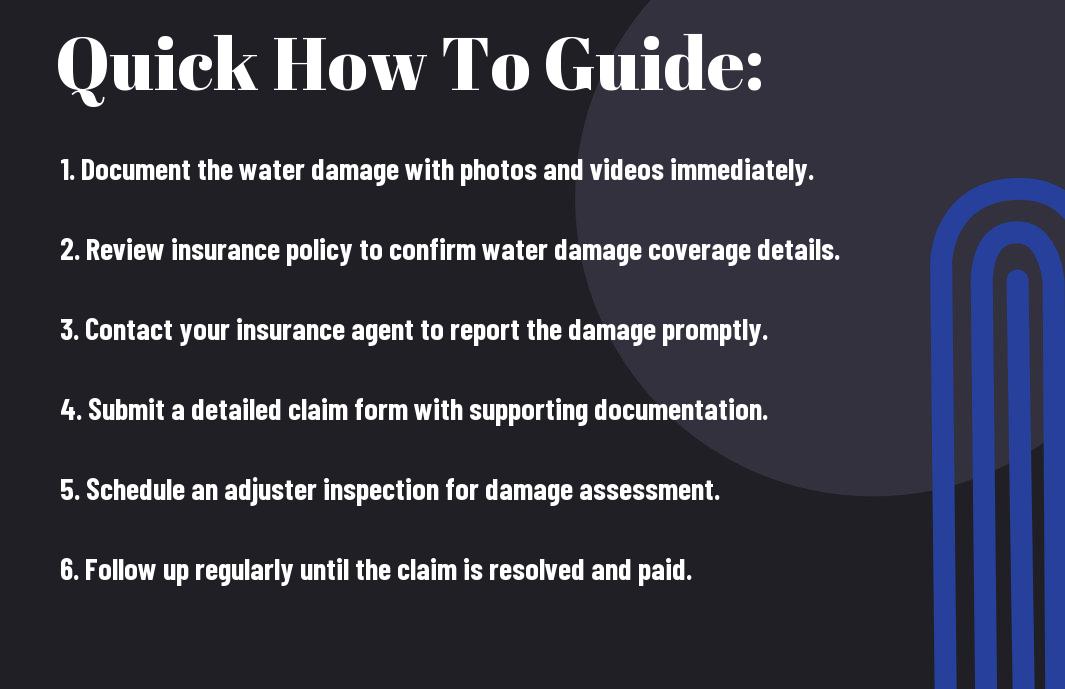

There’s a process to follow when seeking to get your insurance to cover water damage in your home. Understanding the ins and outs of your policy and submitting the right documentation can significantly impact your chances of receiving a payout. To start, you might want to check if your homeowners insurance covers water damage by reading up on Does Homeowners Insurance Cover Water Damage? and prepare yourself for the steps ahead.

Navigating Your Policy’s Fine Print

Analyzing your insurance policy’s fine print could make a significant difference in your claim outcomes. Each policy has specific language that outlines precisely what is covered, under what circumstances, and to what extent. By carefully reviewing these details before a loss occurs, you can better advocate for yourself when it’s time to file a claim. Understanding your coverage fully may arm you with the knowledge to avoid pitfalls during the claims process.

Identifying Coverage Clauses

Coverage clauses are statements in your policy that outline what types of water damage are included. These can vary from flood protection to specific incidents, such as burst pipes or appliance leaks. Familiarizing yourself with these terms helps you understand when your insurer is liable for damages. For instance, if your policy specifies coverage for water damage caused by a sudden plumbing failure, actions taken in response could ensure you receive adequate compensation.

Recognizing Exclusions and Limitations

Exclusions and limitations define what is not covered by your policy and can lead to unexpected surprises during the claims process. Many policies exclude damages from natural disasters like floods or earthquakes unless you have additional coverage. Recognizing these gaps in your policy can help you decide if supplementary coverage might be necessary to protect your investment.

Insurers often specify limitations related to the amount they will cover for certain types of water damage, sometimes even capping payouts. For example, if your policy states it will only cover up to $5,000 for water damage from a specific incident, any cost exceeding that amount will come out of your pocket. Additionally, waiting periods for coverage activation can also pose challenges; a certain period might pass before a claim is honored, which can further complicate immediate repairs. By understanding these exclusions and limitations, you can potentially negotiate better terms or seek additional coverage when necessary.

Documenting the Damage

Thorough documentation of the water damage in your home is necessary for a successful insurance claim. Start as soon as the damage occurs, capturing every affected area and item. A well-documented claim is more likely to be processed smoothly, leading to faster payouts and minimizing your stress during the recovery process.

The Importance of Detailed Evidence

Providing detailed evidence significantly strengthens your case with the insurance company. Comprehensive records help clarify the extent of the damage, ensuring that your claim reflects the true cost of repairs and replacements. This evidence not only supports your claim but also establishes the validity of the damages in the eyes of the insurer.

Taking Effective Photographs and Videos

Effective photography and videography are necessary when documenting water damage. Ensure that your images capture a clear view of the affected areas, showcasing the severity and scope of the damage. Include wide-angle shots to provide context and close-ups to highlight specific issues, such as mold growth or structural harm. Consistently date-stamping photos can further validate your claims timeline.

When taking photographs, use natural light if possible to reduce shadows and clarify details. Capture images from multiple angles to give a comprehensive view of the damage. Your video footage should narrate what is being recorded as you move through the affected areas, explaining the immediate impacts on your belongings or structure. The aim is to create a visual story that complements your written documentation, providing the insurance adjusters with a complete picture of what occurred.

Mastering the Claims Process

Successfully navigating the claims process requires organization and persistence. Begin by documenting every detail, from the moment the water damage occurred to the subsequent steps taken for mitigation and repairs. Keep all receipts and communications with contractors or restoration companies handy. Following these practices will help simplify your claim, reduce disputes, and expedite resolution.

Tips for Filing Your Claim Efficiently

To ensure a smooth claims process, consider these tips:

- Contact your insurance company immediately after the damage occurs.

- Document the damage with clear photos and notes.

- Coordinate with your insurer regarding repairs promptly.

- Submit your claim online or via mobile app if available.

After implementing these strategies, you’ll be better positioned for a successful claim.

Common Pitfalls to Avoid

Steering clear of typical missteps can significantly affect your claim’s outcome. Often, homeowners overlook the specific timelines dictated by their policy, resulting in missed deadlines. Neglecting to take immediate action can also impact your claim—insurance providers may deny requests if they perceive a lack of urgency in repairs. Inadequate documentation holds back the progress of your claim as well; failing to provide thorough evidence can lead to delays or denials.

Additionally, not understanding your policy’s coverage limits can lead to surprises when the claim is processed. Some policies may contain clauses that limit coverage for certain types of water damage. Educating yourself on these unique terms can prevent future headaches. Take a moment to review your policy details before filing and gather ample documentation during the entire process. This proactive approach will help you navigate the claims process with greater ease and efficiency, enhancing the likelihood of receiving the compensation you deserve.

Leveraging Professional Help

Bringing in professionals can significantly strengthen your case for insurance coverage related to water damage. Experts like public adjusters and licensed contractors specialize in navigating the claims process and providing detailed documentation of the damage and necessary repairs. Their experience can ensure that you don’t miss any important details, ultimately improving your chances of receiving the maximum payout from your insurer.

Choosing the Right Adjuster or Contractor

Selecting a qualified public adjuster or contractor is important for support in your claims process. Look for professionals with experience specifically in water damage claims and check for proper licensing and certifications. A good adjuster will not only understand the intricacies of your policy but also argue your case effectively, ensuring all damages are accounted for and claims filed correctly.

When to Consult an Attorney

If you encounter resistance from your insurance company or face disputes regarding your coverage, consulting an attorney specializing in insurance law may be warranted. An attorney can provide insights into your rights and options, assess the legitimacy of your claim, and help you prepare for potential litigation. This step can be valuable when negotiating complex situations, particularly if significant damages are involved.

Engaging an attorney may also be advisable if your claim has been denied or underpaid, or if you’ve experienced significant delays in the claims process. Legal professionals can help decipher the nuances of your insurance policy and enforce your rights, ensuring you’re not at a disadvantage against well-resourced insurance companies. By presenting a thorough understanding of your situation to an attorney, you can strategize effectively for the best outcome with your water damage claim.

Strategies for Effective Communication

Clear and consistent communication with your insurance provider can enhance your chances of a successful claim. Start by keeping detailed records of all interactions, including dates, names, and specific topics discussed. Clearly articulate your situation and the extent of the damage during conversations and follow up in writing to create a paper trail. This approach not only reinforces your case but also ensures that you’re both on the same page throughout the process.

Crafting Your Narrative with Insurers

Building a compelling narrative is crucial when dealing with insurers. Clearly describe the events that led to the water damage, incorporating timelines, photographs, and estimates from professionals. Utilize structured summaries to articulate your position and assert the impact of the damage on your home. This helps insurers grasp the full scope of your situation, increasing the likelihood of your claim being approved.

Following Up: Best Practices for Persistence

Consistent follow-up is vital after submitting your claim. Set reminders to check in weekly or bi-weekly, ensuring that you remain on the insurer’s radar. Document each interaction to track progress and assist in reference during future discussions. If there are delays, professionally express your concerns; your persistence signals your commitment, which could prompt quicker responses.

In addition to regular follow-ups, utilize multiple communication channels whenever possible. Email, phone, and even certified letters can create a layered approach, making it easier to convey urgency. If you do not receive a timely response, politely escalate the issue by requesting to speak with a supervisor. Building a rapport over time can also work to your advantage, as a more personal relationship may lead to more favorable outcomes in the claims process.

Final Words

With this in mind, securing insurance coverage for water damage involves understanding your policy, documenting the damage thoroughly, and communicating effectively with your insurance provider. You should also maintain preventive measures and be proactive in filing your claims promptly. By following these steps and providing evidence of the water damage, you can enhance your chances of obtaining the necessary support from your insurance to address your property issues effectively.

FAQ

Q: What initial steps should I take after discovering water damage in my home to ensure my insurance will cover the costs?

A: After discovering water damage in your home, the first step is to document the damage thoroughly. Take clear photos and videos of the affected areas, including any personal belongings that may have been damaged. Next, prevent further damage by turning off the water source, if applicable, and removing any items from the affected area to minimize loss. Contact your insurance provider as soon as possible to report the incident. Be prepared to provide them with your documentation and a detailed account of the situation. It’s also a good idea to keep records of any expenses incurred as a result of the damage, such as temporary housing or repairs.

Q: How does my homeowners insurance policy typically cover water damage, and what types of water damage are excluded?

A: Homeowners insurance policies usually cover water damage caused by sudden and accidental incidents, such as burst pipes or heavy rain entering through a damaged roof. However, coverage can vary widely depending on your specific policy. Many policies exclude damage resulting from gradual leaks, flooding, or sewer backups unless you have specific endorsements or separate flood insurance. It’s important to review your insurance policy details and understand what is included or excluded, as well as any limits on the amount covered for water damage claims.

Q: What should I do if my insurance claim for water damage is denied?

A: If your insurance claim for water damage is denied, the first step is to carefully review the denial letter for specific reasons provided by your insurer. This will help you understand their decision. You should gather any additional documentation that can support your case, such as evidence of maintenance on your plumbing or further expert opinions on the damage. It may also be helpful to contact your insurance agent for clarification and to discuss the possibility of an appeal. Consider reaching out to a public adjuster or consulting a legal professional for assistance if you believe your claim was unjustly denied.